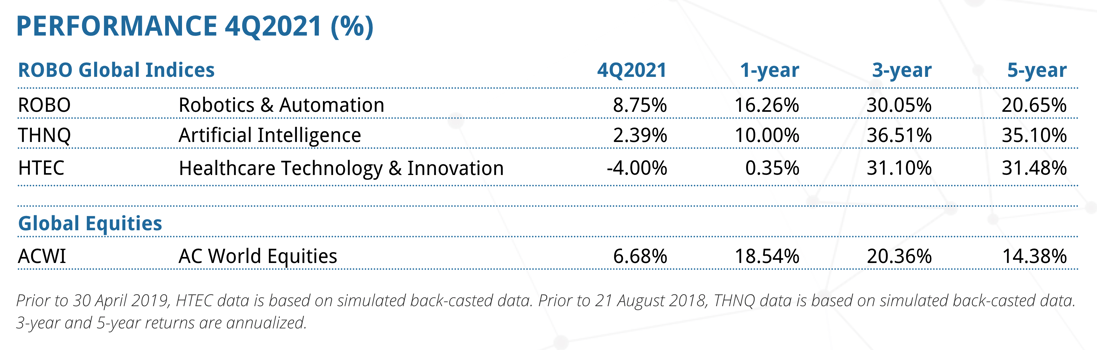

The Robotics & Automation Index (ROBO) weathered the sell-off in many disruptive technology stocks: It outperformed global equities and rose 9% in Q4, to close the year 2021 up 16%. The Artificial Intelligence Index (THNQ) was up 10% in 2021, and the Healthcare Technology & Innovation Index (HTEC) was flat, after both indices rose more than 66% in 2020. While investors debate the near-term growth and inflation outlook, we remain focused on the innovators and market leaders driving these technology trends. In this report, we discuss key developments and big movers across our innovation portfolios.

Webinar Transcript:

Jeremie Capron:

All right. Good morning, everybody, and welcome to ROBO Global's January 2022 Investor Call. My name is Jeremie Capron. I'm the director of research. I'm talking to you from New York. And with me on the call, my colleagues and analysts from the research team, Nina Deka and Zeno Mercer. So we recently published our annual trends research report, which you can find on our website. It's at roboglobal.com. And today we're very excited to present some of the key technology trends that we are watching in this new year and how they relate to our three innovation index portfolios. That's ROBO, the robotics and automation index, HTEC, H-T-E-C. That's the healthcare technology and innovation index. And THNQ, that's T-H-N-Q, the artificial intelligence index. And we will be taking your questions. So feel for free to type them into the Q and a box.

Let me start with a few remarks on the market and our outlook for this year. Our view about a year ago that 2021 would be a boom year that has largely played out. In fact, the global economic rebound has continued. There's a lot of momentum despite the renewed COVID-19 waves and flare ups in the US and the rest of the world with new variants, but I think more importantly for investors in technology, the pandemic has been a very strong catalyst for the digital of the economy and our view that robotics AI, as a next technology revolution, this view has played out at an accelerated pace over the past two years. So think about it. We've all had to make changes to our lives. Our work lives, our personal lives in terms of how we work, how we shop, how we study, how we entertain ourselves. And most of these changes they've been about adopting more digital technology and more automation. And from the point of view of corporations, companies have also had to adapt and where have they been investing? They're digitizing, they're deploying automation and AI at a record pace. And right now the bottleneck is the shortage of workers, which we can see across much of the Western world in China as well.

In the US alone, we've seen the number of unemployed workers back to the pre-COVID levels of just around six million. And in the meantime, we've seen job openings that are searched to more than 11 million. That's a nearly 50% increase from the pre-COVID levels. Whatever the cause is, the immediate answer from companies is productivity. And we believe that this will continue to provide a strong tail end for automation and AI in terms of the demand for solutions around that. And then '21 was a year of shortages. Not only of workers, but also semiconductors. We've seen significant disruptions in supply chains. So essentially you have a constraint supply side and at the same time, you have very strong consumer demand. And so inflation has become a concern. We've seen inflation reaching multi-decade highs and that has triggered concerns around interest for rates.

And in the past few months, investors have been worried about possible hit to economic growth as a result from tighter monetary conditions, tighter fiscal policy. And so we saw very brutal move in some of the most speculative areas of the equity market in recent month. We've seen many stocks that have had extraordinary returns in the recovery from the COVID lows, giving back a lot, if not all of their games. And I think this includes many so-called disruptive technology stocks. So if you look at the NASDAQ, the NASDAQ is down about 8% from the high, but beneath the surface, there's more than a third of the stocks in the NASDAQ index that are down more than 50%. They've been cutting half.

And I want to move to the next slide here. The good news is that our innovation portfolios are not overly exposed to such long duration stocks. And by long duration, what I mean is companies that are loss making, but expected to make significant profits several years out into the future. And in fact, one of the key pillars of our investment strategy here at ROBO Global is diversification. And so while we take the long-term view and we build index portfolios with companies that are positioned to benefit from the technology revolution in the long-term, the index construction methodology is based on a very disciplined system. It's a discipline scoring system to select the technology and market leaders and also discipline weighting system that avoids concentration. And concentration can be very painful as we have seen in recent month. So when we look at our index returns here on the table, we are quite satisfied with the performance of ROBO, and THNQ, and HTEC, and their resilience in this challenging market. In fact, if you look at ROBO in the fourth quarter, the final quarter of 2021, ROBO was up just under 9%. It closed the year up more than 16%. And over the past three years, we're looking at 30% annualized returns. So quite satisfactory here. And you can see on this stable that the three research driven strategies have largely outperformed global equities over the past three and five years.

Okay. Now let's talk about robotics and the trends that we are watching. And then I'll pass it on to my colleagues to discuss healthcare technology and AI. But first, I want to show this long-term performance chart of the index. And again, that's an index that's more than 84 companies right now. They're the best in class robotics and automation companies from all around the world. And you can see here the outperformance over time, which is really a reflection of this ongoing technology revolution, the exponential growth of automation and autonomous systems in pretty much every sector of the economy. On this next slide, you can see that is what we capture with index. The core enabling technologies on the left side like sensing, and computing, and actuation. And then on the right hand side, the most promising applications. And that covers factory automation to eCommerce logistics. You can see healthcare, food, and agriculture, and so on.

So in terms of specific trends that we are paying attention to this year, I would like to start with robots coming to save the supply chain. We all know about the pandemic related supply chain disruptions, but another real important factor here is the dramatic rise in eCommerce volumes. And there's ever shorter delivery times that consumers now expect. And that's driven explosive demand for logistics and warehouse automation. Orders have been exceeding supply capacity for material handling equipment, autonomous mobile robots, the track and trace technology inside the supply chain, the storage system, the retrieval systems.

We think that the logistics and warehouse automation market exceeded $70 billion last year. And we think it will grow to more than 105 billion by 2025. So some of the major beneficiaries in our portfolios are companies like Daifuku in Japan, Zebra Technologies here in the US, GXO Logistics that recently went public. It has very strong presence in the UK. We're looking at AutoStore also recently IPOed company out of Norway, Cardex is in Switzerland. So you can see the breadth here of companies in the portfolio. And we think that really from a technology perspective, it's the advancements in computer vision, in machine intelligence, in materials, in sensors that have really enabled robotics to make a substantial impact in the world of logistics. Today, robotic picking is becoming a reality and we've seen robotic picking speeds now exceeding 100 peaks an hour. And that compares to humans performance just around 60 to 80 peaks an hour. And so automation here is relieving workers from tests that are frankly dull and exhausting and increasingly difficult to find workers for it.

And moving on, I also want to highlight factory automation where we expect to see a surge this year in 2022. In fact, the world's leading robotic companies like FANUC, and Yaskawa, and ABB, and KUKA, they're all ending the year with very inflated order backlogs. They have a strong visibility into demand for 2022, and we expect that the installed base of industrial robots around the world will be just around 3.7 million. 3.7 million robots by the end of the year. And yet that would still represent less than 1% of the number of manufacturing workers around the world factories.

So one of the biggest areas of focus right now is collaborative robots. We call them cobots and they can work seamlessly with humans. And there's an example of that here on the picture in the upper right corner. Cobots are today less than 5% of the market, but we expect the segment to grow by more than 35% per year. And that means a market that could reach 15 billion by 2028. And the market leader here is Teradyne. And Teradyne happens to be one of the best performing stocks. In the final quarter of 2021, the stock was up 50%. Teradyne is essentially a semiconductor testing companies historically. Back in 2015, they acquired Universal Robot and made it the top player in collaborative robots. They have very strong solutions for the supply chain and warehouse automation. And the first nine months of the year, Teradyne sales in Universal Robot, were more than 50% year over year.

I think the third important trend I want to highlight here in terms of robotics is the rise of autonomous vehicles. And here I'm talking about the long haul, but also the last mile delivery. The technologies that are making autonomous vehicles possible are converging and the cost are falling very rapidly. You think about sensors, think about AI and the compute power and communication with 5G now available. That's driving down the cost of goods. We think autonomous vehicles are very promising in terms of potential to speed up deliveries and increase energy efficiency and lower emissions. So today there's just a small number of autonomous cars and trucks around the world. There's many more autonomous mobile robots inside factories and warehouses, but on the roads, we're just getting started. And in fact, Waymo was the first company in the US to launch a fully autonomous taxi service. And it launched in Arizona, but still had a driver up in the front seat. Now, Cruz has just announced that it will become the first company in the US to have a full autonomous service with no driver. So that's becoming a reality. We're looking at companies like Tesla of course, but also Luminar, Nvidia, and Qualcomm that provide the necessary technology to make those systems possible. So Luminar is in lidars, Nvidia is in computing of course, Qualcomm in the umbrella as well. Umbrella that has video processing chips and make some great headway in the auto industry.

Now, China is also leading the way there. And we recently heard from Alibaba that they completed the one millionth eCommerce delivery using autonomous delivery robots. And Baidu also received an approval in Beijing to launch a robotaxi service. So we're seeing autonomous vehicles on the roads. We're going to see more of them. The suppliers of the key technologies are going to benefit. We're also seeing autonomous vehicles on the water. Cargo ships. And recently in Amsterdam, we saw a full autonomous water taxi service start. And also indoor while looking at indoor drones piloting around that we think that's an enormous market opportunity. So I think with that, I'm going to stop here and pass it on to my colleague, Nina. I'd like to invite Nina to talk about healthcare technologies.

Nina Deka:

Right. Thank you, Jeremie. And thanks everyone for joining the webinar today. We really appreciate your interest in ROBO Global. So HTEC is our healthcare technology and innovation index. We focus exclusively on healthcare tech. And this is a portfolio of companies that are basically providing investors with exposure to all the disruption that's happening in healthcare, the high growth companies over the next five to 10 years. So a really exciting time to be involved in this space. Although this chart may not necessarily indicate so in the shorter term given that in the full year 2021, the performance ... the index returned about 0.4%, but if you look at the longer term periods, for example, over a three year period, a back test would show that the index has returned over 30%.

So this is a great long-term opportunity, but also a really interesting time to get involved if you are not yet involved or looking to add positions because right now the index is trading at about 6.4 times forward EV sales, which is a fairly discounted multiple given where it's been historically. For example, last year, it was more in the seven times range. So a really exciting time to get in there. And let me dig in a little bit about what happened last year. So as we're all aware, 2021, a key theme that resonated throughout the year was just uncertainty. Not knowing what was going to happen with the economy, with the pandemic. There was a point where people thought that we were coming out of it and that 2022 be normalized and then Delta happened. And as a result, largely of the Delta variant in terms of healthcare, procedural volumes were impacted. People who were waiting to get their knees replaced for example, once again put that on hold. And so there was already a backlog of people who potentially would've had procedures in 2020 that may have gotten them in 2021 that got further delayed. So this impacted a lot of healthcare companies.

In addition to that, there's the new healthcare worker crisis, which is healthcare worker shortages. During the pandemic, over 100,000 healthcare workers lives have been lost globally. And in the US alone, over half a million people have left their jobs due to various pandemic related reasons since February of 2020. So we all already had a healthcare worker staffing shortage that was growing. It'll continue to grow the gap between people entering the healthcare worker workforce. It seems to be growing because more people are retiring out than people are coming in. Meanwhile, people are living longer. So the demand for healthcare workers in the next 10 years is not going to be sufficient for the number of people say over age 85 who are living longer to receive the care that they need. That dynamic was accelerated in the last year or two due to the pandemic.

So now as we look forward to 2022, we're thinking about what are some areas that are really going to help this issue, which is truly a crisis. When people talk about healthcare capacity, it's no longer about number of beds. There are aren't enough beds available. That's not the issue. That's a 2020 problem. In 2021 and now bleeding into 2022 with the Omicron variant, there's not enough healthcare workers to look after the number of people who need the care. So if we zoom in really quick to Q4, HTEC was down 4% and it was to these indicators that I just mentioned. The Delta variant, procedural volumes being lowered, also concerns around inflation and or rising interest rates. So all these things have impacted tech. And when things impact tech and then things also impact healthcare, HTEC will see both the confluence of both of these factors. Like I said, great entry point for those who are interested.

I do want to highlight two companies that really had a great performance in Q4 of last year. Vocera was up 34%. This is a company that offers a hands free wearable device that is voice operated. As you can see, it's this badge that's worn on the clothing of the two healthcare workers. This company got a lot of attention during the pandemic because it enabled people to communicate with their colleagues, their other healthcare workers outside of the patient's isolation room without having to leave the room, take off the PPE, come back, put on new PPE. So Vocera really helps smooth efficiency and that's just one aspect of what they do. They also offer software that helps integrate all the medical devices in the hospital. And on that health handhold device, a physician or a nurse can get all the updates without having to go to the patient bedside.

So given their ability to integrate and have this underlying software that kind of ties together all of the devices in the hospital. We not only saw this as an attractive investment opportunity, Vocera is a member of not just HTEC, but also of ROBO. It was just announced a few weeks ago that Striker, another company in HTEC, plans to acquire Vocera. And this is a pretty attractive valuation here. It was about 10 times next year's sales, which is a premium given, but it was warranted given the sophistication of this company's analytics and integration capabilities. We expect to see the investment trends toward healthcare, data analytics, and integration capabilities. This is just early days. Healthcare just went electronic in the last 10 years. There is still a major opportunity for a lot of disruption here. So this is just one example of why, although healthcare tech looks like it took a little bit of a backseat, there's still so much here that is going to be forward looking at a lot of upside in terms of valuation and multiple expansion.

Another exciting company in Q4 is Codexis. Codexis returned 34% in the quarter. And they reported an increase 242% revenue in the previous quarter due to 29 million in sales from their partnership with Pfizer. It's been widely reported that Pfizer has an antiviral remedy for coronavirus for COVID 19. And so Codexis is a company in the HTEC index that Pfizer partnered with to provide the proprietary enzyme used to make the drug. So I want to highlight here that this is just one company of many in the index that are enabling a lot of technology and healthcare to move forward. These enabling companies are ones that not a lot of people have heard about. There's other examples of it like Moderna and J&J both partnered with Catalent to get their vaccines out the door. And Lonza. Catalent, Lonza, Codexis are all examples of companies that are third party manufacturers of drugs. And they provide very sophisticated level of manufacturing capabilities. Think about mRNA. Nobody had ever heard about it, well, outside of the science community until last year or the year before. And now it's a multi-billion dollar business. And it requires a level of sophisticated to be able to manufacture that at scale, and Catalent rose to that occasion.

So these are just examples of when you see something really cool happening in healthcare in the news, chances are those companies probably had to partner with other companies. And so there's a lot of opportunity for investment upside here. And so really this is where if you're interested in capturing all that upside potential, a diversified portfolio might be a good strategy for you. And so that's what HTEC offers. So as we look forward now into 2022, I mentioned that what we're going to be-

Erin:

Nina?

Nina Deka:

... keeping an eye on.

Erin:

Apologies. Can I interrupt you just really quick? Because we have a question to explain the huge underperformance of HTEC compared to global healthcare index. So before you move into the forward looking, could you kind of address that really quick?

Nina Deka:

Oh, absolutely. Thanks for the question, Erin. So essentially, as I mentioned, when healthcare and tech take a hit, that will impact healthcare HTEC a little bit more than the global healthcare index. So if you were to look at ... And actually we have a slide that describes this area with the horizontal bars. If you were to look at the global healthcare indices, the large ones like S&P, what you'll find is that they're much more heavily weighed in large cap pharmaceuticals and hospitals, health insurance companies. The reason why is because those portfolios are cap driven. They're comprised largely of large cap companies. And the largest cap companies in healthcare are large cap pharma and health insurance companies. And that is a very different investment strategy.

We have less than one-fifth overlap with those types of portfolios. So during a time of uncertainty when people are concerned about things like inflation or rising interest rates, they tend to migrate towards some of the more value investment opportunities companies with growing dividends and companies with positive earnings, positive cashflow while solid investment opportunities tend to be growing in the single digits. And like I said, that's a very different investment opportunity. If you look at the green bar, the green horizontal bar, this is the HTEC. So as you can see, HTEC is a little bit more ... very much more diversified across these other areas that we believe represent all that technological growth and disruption that I was just describing to you. So companies that are helping to manufacture mRNA, companies that are helping to integrate all the medical devices in a hospital, 3D printing, surgical robotics, genomics, diagnostics. If you look looking for more diversified portfolio that's going to cover those parts of healthcare, like I said, that's what HTEC has more comprised of. However, in an environment where people were more concerned about high growth tech names companies that might not have positive earnings, but expect you in the next couple of years, those stocks over the last year basically took a hit. And so HTEC saw the confluence of that.

And then I mentioned earlier the level of excitement we have around companies providing data, that's data analytics and AI. There is a lot of dysfunction happening in healthcare right now. So if you were to think about why should I invest in healthcare innovation right now? I think one reason not to invest is if you think healthcare is fine the way it is. If there is no healthcare worker shortage, if everything's fine, if there's no medication related errors, everything's going smoothly, then there's not a lot of room for disruption, but we know that that's not the case. And so one way that we're going to be able to solve all these problems is through data analytics and further integration.

Another really interesting company is called Health Catalyst in the HTEC portfolio. This is another data analytics company that's integrated with hundreds of software programs throughout a hospital system. And they can analyze a population in an area and provide data to the hospital and say, "Look, we see an area where people are at risk of being hospitalized because of their high risk health situation." Health catalyst will help consult with the hospital to provide a plan to be proactive and go after the high risk population. And in doing so in one particular hospital, they were able to help save $32 million and lower patient admissions because just from identifying ahead of time using analytics and AI to see which of the population they can serve and help keep healthy and prevent the illness to begin with.

Another really exciting area that we're following as I mentioned is robotics. When I talk about how there's a healthcare worker shortage, one of the ways that we're going to be able to approach this and move forward is through automation and companies providing healthcare robotics right now are really on fire. There's one in the HTEC and ROBO portfolio called Omnicell. Omnicell provides robots to pharmacists and to hospitals to help automate the pharmacy process. If you think about pharmacies today, you've got a pharmacist putting pills in bottles and then doing a ton of administrative work. And yet 90% of pharmacists indicate in a survey they can't find enough help to do all the work that's needed. Meanwhile, medication error is the third leading cause of death in the United States. So we've got an issue here and a huge opportunity for automation. And Omnicell is a really interesting company right now, and they are also growing and did very well last year.

And then another area we're really excited about is spatial biology. So this is something that we think is going to be the next frontier in genomic science. Next gen sequencing was a really big deal in the mid 2000s onward. We saw a huge inflection point there when they started being manufactured and we believe that that's going to be happening, spatial biology. We expect to hit an inflection point similarly in the next year. And if you want more details on spatial biology, happy to talk about that further. And we also have details about that in the report. I'll just say very quickly that what spatial biology does is it allows you to have a snapshot of what's going on, for example, inside the body, like within a tumor at more detail than if you were to just simply sequence ... do the gene sequencing.

If you were to think about a map, picture a map with no streets and no addresses. What spatial biology does is it basically puts the addresses, and the locations, and the building numbers on the sample. And so if you think about that in a tissue sample, it's giving you just a lot more detail than you would've otherwise had. And with this, people are going to be able to develop better therapies and also diagnose cancer better and other illnesses. With that, I'm going to pause and actually pass it over to Zeno who's going to talk to you about THNQ, our AI portfolio.

Zeno Mercer:

Thank you, Nina, for covering HTEC. Hey, everyone. Today I'm going to be covering our THNQ index. That's T-H-N-Q. And within THNQ, we essentially are trying to capture the universe of artificial intelligence from application to infrastructure from the ground up. So across applications, we've got cloud provider, network security, semiconductor. So these are the platforms that are ... and hardware that are providing the brands for the applications that we now take for granted essentially to even work together. And on the application side, we see exciting companies across consumer facing eCommerce especially increasingly in the last year healthcare and business processes is we see cloud adoption across companies. A lot of it induced from the COVID pandemic. And additionally, we also see factory automation. So the think index had a ... we'll admit it had a rough quarter for the Q4. It was up 2.39% and up 26% on an annualized base since inception. So there was a mix of factors that contributed to this performance. And some of it being just fears around tapering and the interest rate environment impacting some of the higher growth stocks. But that being said, we're seeing the demand for AI and adoption from the network level, from the application level has never been higher.

So we've got data coming in from autonomous vehicles, augmented reality, all these new platforms that are being deployed in the real world actually with real business functions. We've got rising the cost and energy. There's a big demand for maintaining energy costs, both at the data center level and micro device level, that could be laptops to giant data centers providing AI for drug discovery. And then we've got the economic benefits. That it's one thing to consider. The AI is changing every industry. There isn't a decision made at a Fortune 500 company now that isn't driven now with data and analysis. And then furthermore, that is getting down into the products that are being deployed to customers, both enterprise is and consumer. Real quick. Could you go to the applications and infrastructure page? Yeah.

So I just want to highlight further on performance. So Semiconductor network security had a great quarter. Nvidia and A&D both saw slightly over 40% stock returns. There have been a lot of concerns around the ability of these companies to deliver. And about a year ago, everyone was kind of concerned, will they be able to keep up demand? Will they have supply chain issues that prevent them from making money? And the answer is yes. They delivered on all the above and demand has never been higher as increased applications and companies getting ready for 2022 and beyond are utilizing these platforms. Healthcare technology companies and big data analytics, as we already discussed, saw a little bit of a laggard and large deployments saw some pushback. Once again, this is in the 2022. So this impacted. These company is not semiconductor. And then lastly, high growth FinTech, which is a portfolio, a part of our portfolio that we'll talk about a little further on, was hit hard as similar concerns around inflation and rising interest rates. But in the longer term outlook, we see massive continued adoption here.

Now onto the company highlight here, Arista networks led by CEO, Jayshree Ullal, is a cloud networking provider that is powering large data centers from Microsoft, Google, Amazon. And essentially they provide these networking switches that allow them to communicate and run faster at more energy efficient. These data centers consume a lot of power, lot of compute. This is a platform that won't be in the news for consumer product or anything. They are very important, very powerful. As I mentioned, it was up to 67%. It's a strong cloud environment. And they raised their expectations to 30% and growth in 2022 even with continued supply chain issues. So once that subsides, you're going to see even more tailwinds there. And then New Relic, a company I'm sure most of you are probably not familiar with because it's mostly developers and cybersecurity experts utilizing this, but it provides full stack analysis for both the infrastructure and application, which is very important because a lot of players out there just look at one or not the other, and you really require both of them working at the same time to be able to operate. Companies like Uber. Just any company out there that relies on massive data sets and realtime analysis and suggestions needs this type of analysis.

Think about how your car runs. That's just a single environment with sensors. We're not even talking about autonomous vehicles here. It needs to understand how the oil, the gas and all these things are running. This basically provides that, but it goes beyond that for much bigger applications. One of the reasons for their massive growth in the fourth quarter was they not only just beat expectations, but they also announced that they scored a $3.5 billion new customer, which is one of the largest ever. And they announced two new products that should increase the acceleration. And now I'm going to cover some trends that we're excited about going forward in 2022 and beyond. So AI machine learning driving the multi-cloud adoption. So what does that mean? As I mentioned, while front-end applications get a lot of the attention, multi-cloud environments are that middle and back layer that empower this transition to the digital world. The goal is to make these interactions as seamless and reliable as possible, whatever the scenario across autonomous vehicles, the metaverse, any autonomous. So if the rising tide is the demand for these services, then the water really, the poll is ... that's enabling this is the multi-cloud networking environments. So ultimately what you should take away from this is the ability to securely share data and store data across different platforms, and then analyze it with different services is paramount as we get into increasingly complex scenarios.

Gartner actually expects the global cloud market to grow to 402 billion in 2022, which is 35% higher from 2021. So we're seeing massive growth spend here. And index numbers such as JFrog, Arista Networks which I just mentioned, MongoDB, and CloudFlare massively benefit from this trend.

Next topic and trend that I want to cover is next generation banking. So banking and finance, as we know, is transforming. Technologies across blockchain, digital assets, utilizing technology such as voice recognition, better identification, and cybersecurity are helping automate both backend and consumer experience processes. So this is going to provide a massive transformation to banking services and eliminate some overhead, but it's really possible due to machine learning enabling more accurate predictions risk management, enabling better consumer interactions. So this is going to cover insurance, fraud, mortgages, cashless payments, digital insurance. There's really not an area this isn't going to touch eventually. And this isn't just theoretical. These are being deployed and utilized right now out with both private and publicly traded companies, such as THNQ index members, Lemonade, Upstart, Fair Isaac, and Block, which if you aren't familiar it’s Square just rebranded this past year to reflect more emphasis on blockchain. These are all leaders in digital banking that we are excited to see grow in 2022 and beyond.

The last trend I want to cover is kind of a combined a metaverse and immersive experience. Now this really impacts all of our indices, but AI is the crux of this. Sure. You might think of just putting on a headset is not really AI, but you've got to be able to rapidly analyze the data coming with computer vision and sensors. You have to send that data off somewhere using 5G where it's synthesized and analyzed to provide you real time content. So I think a lot of people wonder what will metaverse touch and impact. I think it's what won't it touch? What will it replace? Would you rather have a cell phone or augmented reality contact lenses or glasses? Besides philosophical areas, I think we can all agree we've spent too much time looking down at a phone and touching. So some applications that we're looking at and excited about are education, healthcare, coaching, games. Those are some of the more consumer focused. On the other side and equally as important, we're looking at manufacturing, and production, and new types of products that are more energy efficient, sustainable, and just overall better, and safer for the environment. This real-time feedback and personalized experience requires immense data sets and analysis and throughput. So index members and semiconductor companies like Nvidia, Taiwan Semiconductor, AMD are providing a lot of the raw horsepower here. But this also requires a lot of design and applications.

We have to essentially recreate the digital or the physical world in the digital world here to be able to understand it. And so companies like Adobe, Dassault, Autodesk are powering a lot of the innovation here. For example, the Dassault is working in a number of different fashions, digital virtual twins that represent your own body. So this can be used across healthcare, across just self-analysis and wellness trends, things like that to give you a better snapshot and actually build application layers on top of that. Another one, if you look at the bottom right corner, you'll see a guy wearing a headset, and that's a collaboration between two THNQ members, Microsoft and Trimble. And they're working to provide frontline workers with a functional helmet with an augmented reality overlay to get real time information and communications without having to use another device. Imagine they're up in a building. They don't need to be dealing with that. It's a seamless overlay. And this is a live product now getting deployed, which is incredible. So that being said, I think we're going to move on to Q&A. Feel free to ask any questions around anything we've covered.

Jeremie Capron:

Okay. Thank you very much, Nina and Zeno. I see we have quite a few questions coming through the box here. I want to remind everybody feel free to type your questions in and we'll try to address as many as possible. I want to kick off with some of the questions I've seen around investing in companies with no earnings in the current environment. I think that's a very good question. It's really important given the change in the market regime that we've witnessed over the past a couple of quarters as inflation started creeping up. We're starting to see what kind of shape the monetary policy responses is going to have. As I said in Q4, Q4 was brutal for many so-called disruptive technology stocks, but if you look under the cover, you look at what stocks have come down or come crashing down in many cases. Those are the stocks that I would qualify as some of the more speculative names out there, companies that have very ambitious plans, and promises of earnings that are very far out into the future. And in the meantime, they're burning cash and they're scaling. The good news is that in the ROBO Global portfolios, you are not going to find extreme exposure to those names.

We do own in those industries some companies that have no earnings today, but they're the exception rather than the norm. In fact, and is something that we quoted in the annual index review report that we just published yesterday, if you look at ROBO, the number of stocks that have an EV to sales multiple above 10 times is around 15. So there's 15 stocks out of a total 84 that trade on a high revenue multiple, and that's indicative of very little to no earnings. And so that's about 20% of the portfolio, but at the same time, there's another 10 stocks that are trading on an EV to sales multiple of less one time. And so that should really help you understand that the diversification that we have in our portfolios. And that's a really important pillar of our investment strategies for all three thematic indices. And so ROBO actually outperformed global equities in Q4 because the hit it took in some of the higher multiple names was largely offset by the rotation into the more cyclical and the more value areas in the market. So when it comes to robotics automation, those value or cyclical areas are typically found in factory automation. Those are more cyclical names. It tend to be capital goods types of companies.

A lot of them are in Japan. And the Japan piece of ROBO portfolio is largely underperformed in the first part of last year and it's starting to catch up. In fact, in 2021, our Japanese holdings were flat year over year when the index itself was up 16%. We're not overly concerned about what's happening in terms of the rotation in the equity market now. We think the indices should be relatively resilient. I think Nina can comment on the number of companies that are not profitable today in a healthcare technology and innovation in that will give you also a good sense of that. Nina, can you take over here?

Nina Deka:

Absolutely. Yeah. So about 33% of the companies in HTEC are not yet profitable, but when we analyze companies, we are looking for a clear path to profitability or some sort of clear path to revenue. If you look at the HTEC portfolio, most of the companies trade on a multiple of EV to sales or even a multiple of EBIDA. So we're looking at either there essentially the investment opportunity there is in growth or also in some sort of clear direction toward cash flow, which we believe EBIDA would be the representation of that. Yeah. The vast majority of the companies do have earnings. And so we do feel that that is fairly de-risked from a technology and innovation basket standpoint.

Jeremie Capron:

Thank you, Nina. I see a lot of questions related to the index and portfolio construction methodology, the rebalancing strategy and the weighting of constituent. So I'm going to start off here and ask Nina and Zeno to comment as well. But essentially what we do here is we combine the benefits of active research in terms of selecting best in class companies to express our bullish view on the themes. That's the first part of the work. And it implies a lot of analysis and scoring of each and every company in our universe. And then we combine that with the benefits of index investing, the various investment vehicles that can track indices in terms of the risk management, in terms of having a quarterly rebalancing to maintain that modified equal weighting across the portfolio throughout the time and not for a long period of time.

So the result is that you have diversified portfolios because the weightings for each constituents are typically somewhere between 0.8% at the low end all the way up to 1.8%. And because we balance every quarter, we reset the weights to that score driven weighting. And that means that the index will sell the biggest winners at the end of the quarter or towards the end of the quarter and will buy the biggest losers, assuming that those companies continue to score very high on our methodology and that we want to own them for the long term. So that kind of embedded risk management process really enables us to avoid some of the biggest pitfalls in disruptive technology investing. And as we saw in recent month, this can be very painful when you are overly concentrated in a handful of names or in one very particular subset of the theme.

I think a great example of that is what happened with gene editing and genomics in general. I think Nina can comment on that. We've had a really phenomenal year for genomics in 2020 with some big developments and essentially confirming the feasibility of using the CRISPR technology, for example. And then last year, those genomic socks and CRISPR in particular came to earth in terms of for reconnecting with the value of the underlying fundamentals. So Nina, why don't you comment on the gene editing and precision medicine in general? I see we have a few questions around that too.

Nina Deka:

Sure. So I didn't actually see what the questions were. I want to make sure that I do to them. So if I don't answer them, feel free to reprompt me again, but essentially last year or the year before, I mentioned earlier mRNA as an opportunity. We've only now seen one type of mRNA therapeutic come to market and become commercialized. There are so many others currently in the pipeline. In fact, Moderna, another company in the HTEC portfolio, had over 20 different therapies in the pipeline before the pandemic even happened. And what we've seen historically is when a new therapeutic modality has success, then adjacent companies or other candidates that are in clinical trials or pre-clinical, we tend to see positive movement adjacencies to those stocks as well. But we particularly like Moderna because they were the lead in terms of the number of other candidates in clinical trials.

So before the pandemic, they were working on a vaccine for HIV, for Zika, for CMV, which continues to progress. It's in phase three right now. And now that one has come to market, that whole modality has been de-risked. And so that is a positive catalyst for basically every other mRNA therapy that people are working on right now. I also want to point out from Moderna that they're very rapidly working on a flu vaccine and this could be game changing. They want to quickly bring one to market by sort of following conventional methodology, bringing basically a normal flu vaccine to market. What that means is that every year the WHO provides a list of what they believe the next year's flu strains are going to be. And pharma companies need eight, nine plus months to manufacture this drug and bring it to scale in time for the flu season for each hemisphere. Well, that's a long lead time. And often, the strains that are predicted to be the dominant strains of the flu season don't wind up being the case. And that's why we don't see a ton of efficacy around flu.

Moderna is working on basically a game changer maybe in the next couple of years. They want to have one because it only takes them a couple of months to get a drug through clinical trials or at least to prove that it works. And so if they can get a flu vaccine approved that only needs a couple of month lead time, then they can actually develop one closer to flu season and it might have much higher efficacy. This could be game changing for the whole healthcare industry for the whole world really because hundreds of thousands of people die from the flu. And eventually they plan to combine that with COVID and have a combined vaccine and maybe even include RSV, another vaccine that they're working on, but tons of other things are happening.

I mentioned earlier spatial biology. Precision medicine is an area where therapies are being developed to treat very specific genetic mutations. And if you can identify, "Okay. Here's the gene the that's causing this cancer." You can come up with a therapy to treat that very specific cancer. With spatial biology, you can also determine how effective a drug can be because you can see other genes nearby that might interfere with a drug's ability to be effective and actually come up with an even more personalized formula, if you will, or a more personalized therapy. This will also be game changing as we look to the future and expect drugs to get more and more personalized. That's going to be enabled by companies like Roche and other company in our portfolio with all of their advancements. And then there's a ton going on in terms of early cancer detection. Over 10 billions of dollars have been invested in M&A for early cancer de detection in liquid biopsy in the last couple of years. So a really exciting space there. The market is expected to be well over $30 billion and people will have the opportunity in the future to potentially detect cancer sooner than they otherwise would've been. And an estimated a 100,000 lives per year in the US alone could be saved with earlier cancer detection and much greater around the world.

Jeremie Capron:

Thank you, Nina. I see we have a few questions on AI. So I'm going to invite Zeno to speak one or two and address them.

Zeno Mercer:

Hi, Everyone. Yeah. I saw a couple questions around ... a couple questions and comments. Someone commented, "Somebody predicted this back in the day." You've got questions like, "Why hasn't AI or metaverse predictions ... why have they failed to materialize?" And one of the things that I want to point out here is there's a saying, people tend to overestimate what can be done in a year and underestimate what can be done or five and 10 years. And I think what we're seeing here is that people saw the vision of a lot of these things. Once computers were around, once people realized that there could be something that can also think and make actions and decisions, people theorized that we would be getting to this point. Maybe not exactly how, or when, or all those things, but there's always predictions. And we're actually seeing a lot of these things come to light right now, as I mentioned. We've the metaverse, we had Google glasses, I forget, over a decade ago now at this point for a couple little applications manufacturing, it wasn't there yet. A lot of the, we'll call it the weakest links. The ability to provide smaller pixels, more transparent screens. There there's a confluence of materials, hardware, energy efficiency, which is huge. The chip and energy efficiency for the form factor.

A lot of this is just progress by progress. Each incremental innovation stacks on to provide an innovation somewhere else. A more energy efficient battery allows a drone that normally couldn't have flown around, to be a consumer drone to check things around. That's suddenly feasible. And so switching back to the metaverse and the applications, we're at the tipping point now. 2022 as we predict it to trend, it's happening. Now, it's going to start more in higher risk higher areas just kind of in the film industry. The film industry, they traditionally filmed aerial views with helicopters. So the first place to adopt drones was the film industry because there was an obvious value with the low risk of adoption. And so that being said, we're seeing that now the same thing, manufacturing. Other high risk areas that have a huge problem to solve, but it's trickling down. You've got Facebook, AKA, Meta. Their glass is to record your events in your life. And so as we get to each level, you're going to have heads up displays that almost anyone can have.

Students might have glasses that the teachers monitor and instead of separating physical education and education itself, you might be able to having them interact, and visualizing, and participating and you'll get more personalized experience in education for kids around the globe. You don't have to be in the classroom anymore when you have that immersive experience. So we're just going to see this massive transformation and investment into these spaces.

Somebody also asked about geographies. Even on our portfolio, a lot of our portfolio weighting is in the United States. There's no question. Most of the innovation across all of our portfolio indices are coming out of the US. A lots of research comes out of universities, companies, it trickles up. Obviously though robotics and AI, we're looking at Japan, and China, and other areas as well. Great ideas innovation come from anywhere, but we're still heavily weighted in the US for that.

Jeremie Capron:

Okay. Thanks very much, Zeno. And I'm going to thank everybody for joining. We are running on the hour just now. So we'll wrap it up. Thank you very much for your interest in ROBO Global. You can visit our website, roboglobal.com if you want to sign up for biweekly newsletter in which we share some of our research from companies, and trends, and the indices that we build. And with that, I wish everybody a very good day. And we look forward to talking to you again very soon. Goodbye.